If it’s been a while since you engaged with your pension, the tax year end is a great time to review your contributions and make the most of allowances that will reset on 6 April.

Pensions are one of the most tax-efficient ways to save, so maximising your annual contributions could help you accumulate the wealth you need to turn your retirement ambitions into reality.

Keep reading to discover three important reasons to boost your pension pots before the tax year ends on 5 April, plus the rules you need to remember.

1. Reduce the risk of being dragged into a higher Income Tax band

Before the 2021/22 tax year, Income Tax bands typically increased in line with inflation. However, in 2021, the government introduced a freeze on personal tax thresholds.

In her 2024 Autumn Budget, the current chancellor, Rachel Reeves, confirmed that this freeze will remain in place until April 2028.

This could increase the risk of “fiscal drag”. In other words, if your income and inflation rise, a larger proportion of your earnings may fall into higher tax bands. As such, your tax burden could increase, even without an explicit increase to tax rates.

Indeed, the Guardian has reported that the number of higher-rate taxpayers rose by almost 2 million between 2021 and 2024 due to the freeze on personal tax thresholds.

You might be interested to learn that increasing your pension contributions could reduce your taxable income, potentially allowing you to avoid being dragged into a higher Income Tax bracket.

For example. Imagine that:

- You earn £150,000 gross a year

- You make £30,000 gross pension contributions before the end of the 2024/25 tax year

- Your net adjusted earnings would fall to £120,000.

As such, you would not need to pay the additional Income Tax rate of 45%, which applies to earnings over £125,140.

You can contribute up to £60,000 (your Annual Allowance) to your pension tax-efficiently in

the 2024/25 tax year. Your total contributions must also be less than or equal to your annual earnings

So, if you have not yet used your full allowance, it might benefit you to do so before 6 April when the new tax year begins and your allowance resets.

It’s important to note that your Annual Allowance may be different if your income exceeds certain thresholds or you have already flexibly accessed your pension. If you exceed your Annual Allowance, you may face an additional tax charge.

You can also carry forward unused Annual Allowance from the last three tax years. So, if you want to contribute more than £60,000 to your pension before 6 April, it’s worth checking with HMRC if you have any Annual Allowance remaining from the 2021/22 tax year and beyond.

Remember though, that pension wealth is usually locked away until you reach 55 years old (rising to 57 in April 2028). As such, before boosting your pension pots, ensure you have sufficient funds to cover short- and medium-term expenses.

2. There is no longer a lifetime limit on how much pension wealth you can accumulate

The Lifetime Allowance (LTA) was a limit on the amount you could build up in pension savings without incurring a tax charge.

The LTA stood at £1,073,100 in the 2023/24 tax year. If you took a lump sum at the point of retirement, you’d usually pay tax at 55% on any amount that exceeded the LTA. If you withdrew funds as income, you’d pay 25% (on top of regular Income Tax).

As a result of these tax charges, you might have stopped making contributions to your pension pots if you were nearing or reached the LTA.

However, the LTA was officially abolished on 6 April 2024. There is now no additional tax charge for accumulating a large pension pot.

However, this doesn’t mean you can take more from your pension without paying tax, as the LTA was replaced with three new lump sum allowances that cap how much you can withdraw tax-free. Also, the maximum amount of pension contributions you can make in a single tax year is limited by your income and the Annual Allowance, as described above.

Read more: 3 new pension allowances you may need to know about in 2024

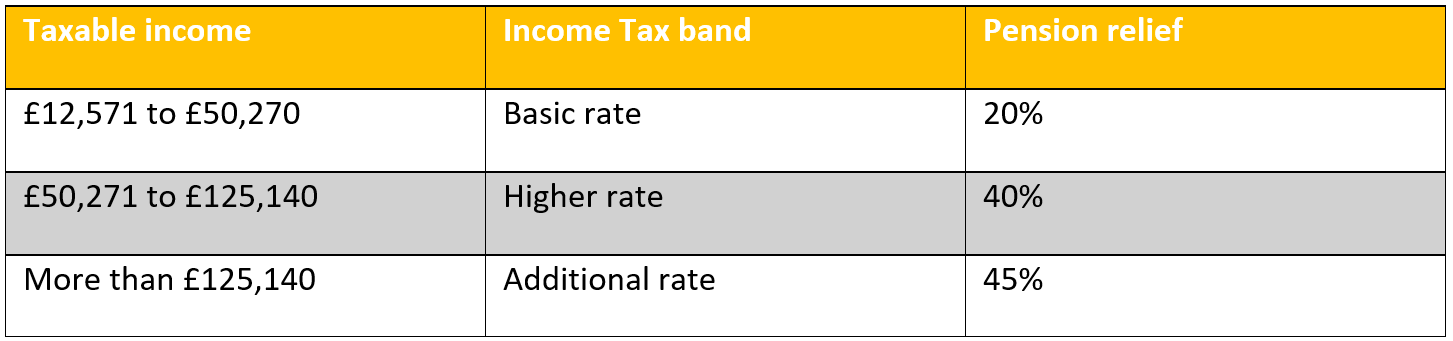

Although there are still limitations in place, your pension offers an attractive way to save due to the removal of the LTA, and the tax relief you might get on contributions, detailed in the table below.

The basic-rate relief is applied automatically when you or your employer pays in. If you’re a higher- or additional-rate taxpayer, you may be able to claim an additional 20% or 25% respectively through your self-assessment tax return.

So, if you previously stopped making contributions because you were approaching the LTA, you may want to resume making tax-efficient contributions to your pot.

Remember, the clock is ticking for making the most of your Annual Allowance before the end of the tax year.

3. Retain your full Annual Allowance even if you’re a high earner

As you read earlier, the standard Annual Allowance is £60,000 for the 2024/25 tax year. However, your allowance may be reduced if:

- Your “threshold income” exceeds £200,000 – This is your income minus pension contributions made by you or a third party (not including your employer)

- Your “adjusted income” is over £260,000 – This is your income plus the amount your employer pays into your pension, or the amount your defined benefit pension has grown by, if you have one.

- You take money out of your defined contribution pension and trigger the Money Purchase Annual Allowance. This limits the amount of contributions you can receive tax relief on to £10,000 a year.

If both your threshold and adjusted income exceed the above thresholds, your Annual Allowance will be reduced by £1 for every £2 you earn over £260,000 until it reaches £10,000. This is known as the “Tapered Annual Allowance”.

This example from Money Helper shows how the Tapered Annual Allowance could work in practice.

- Imagine you earn £250,000 a year in total and pay £30,000 into a pension.

- Your threshold income would be £220,000.

- If your employer also contributes £30,000 to your pension, your adjusted income is £280,000.

- As this is £20,000 above the £260,000 threshold, your Annual Allowance would be reduced by £10,000 to £50,000.

- However, if you make enough personal pension contributions to reduce your threshold income to £200,000 or less, your full £60,000 Annual Allowance could be reinstated.

As you can see, the rules surrounding your annual tax allowances and the associated calculations can be complex.

If you want to boost your pension before the tax year ends on 5 April, you might benefit from speaking to a financial planner who can help you make the most of your allowances.

Get in touch

If you’re looking for a financial planner in Bristol to help you manage your pension wealth as tax-efficiently as possible, we can help.

Please get in touch either by email at helpme@aspirellp.co.uk or by calling 0117 9303510.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Workplace pensions are regulated by The Pension Regulator.

Production

Production

of clients believe that working with us has helped or will help them achieve their financial goals

of clients who answered definitively said they would recommend us to their friends, family or colleagues

of clients said they were satisfied with our communications during times of market volatility.